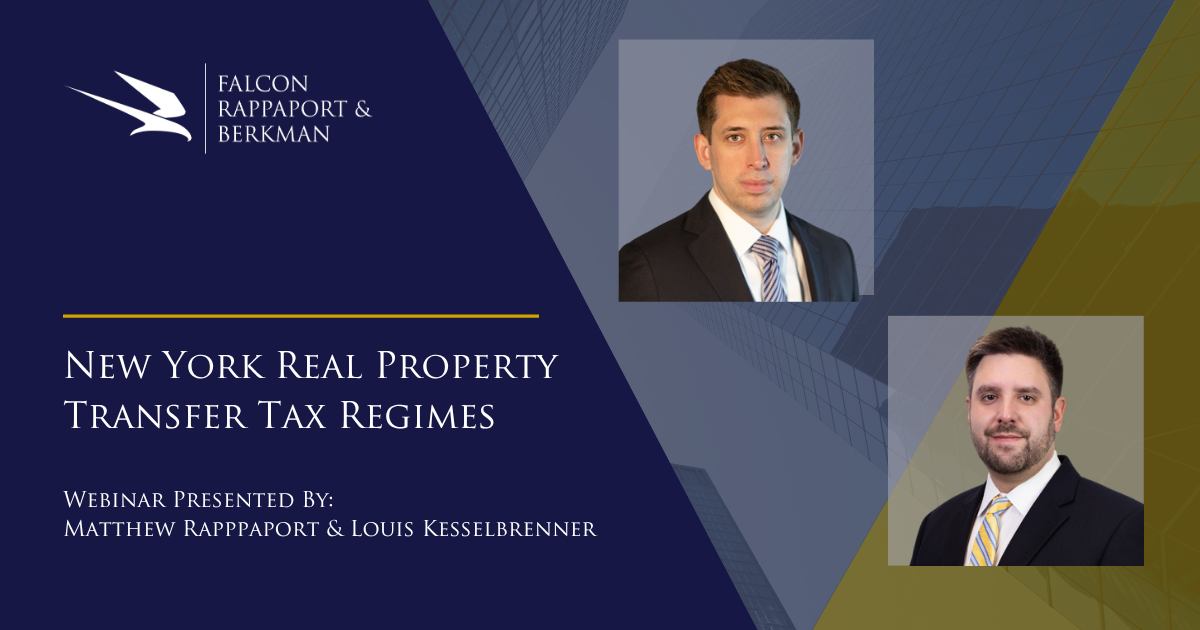

We recently hosted an in-depth webinar examining one of the most nuanced and frequently misunderstood areas of New York real estate taxation: New York State and New York City Real Property Transfer Taxes. Led by...

Falcon Rappaport & Berkman is proud to share that Vice-Managing Partner Matthew E. Rappaport was quoted in a Wall Street Journal article by reporter Richard Rubin, “America’s New Tax Mantra: ‘The...

Falcon Rappaport & Berkman is proud to announce that Matthew E. Rappaport has been selected as a 2025 Outstanding Faculty Award recipient by the National Business Institute (NBI). NBI is one of the...

By: Matthew E. Foreman, Megan E. Wilson, and Bristol Francis Introduction Effective December 24, 2025, the United States Postal Service (“USPS”) amended the Domestic Mail Manual (the “D.M.M.”) by introducing section...

Falcon Rappaport & Berkman is pleased to announce that Vice Managing Partner Matthew Rappaport and Co-Managing Partner Moish Peltz will be speaking at the Capital Events Summit 2026, an invitation-only breakfast...

By: Angela M. Stockbridge, Esq. For many years, employers and benefits professionals have treated voluntary benefits such as accident, critical illness, cancer, and hospital indemnity insurance, as a relatively low-risk...

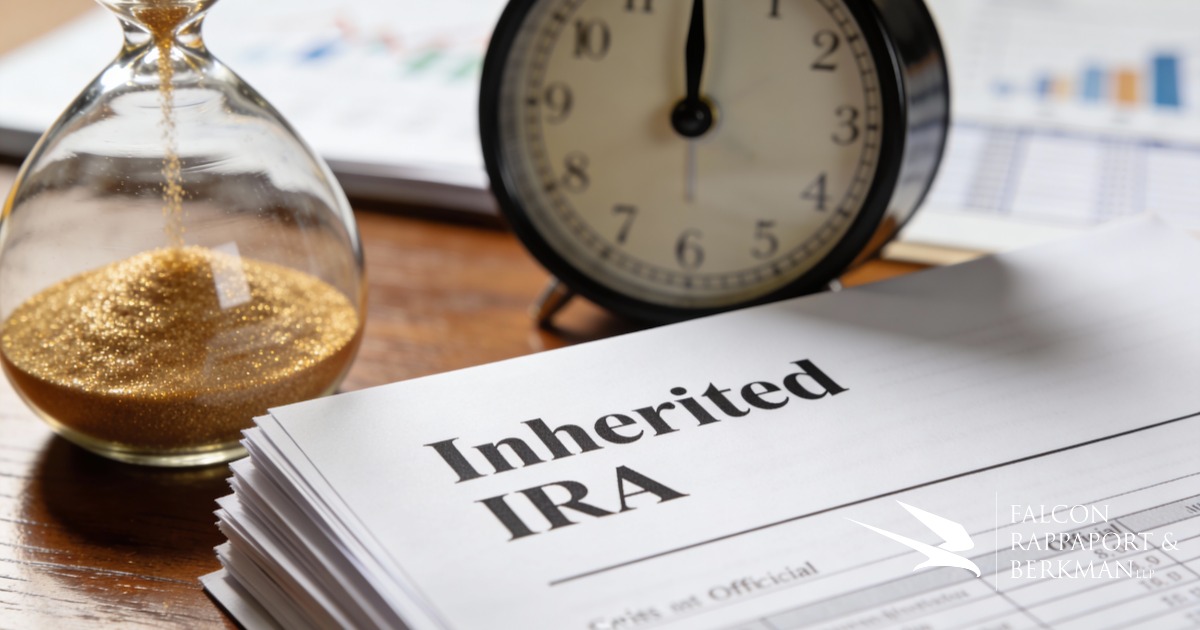

By: Angela M. Stockbridge, Esq. A recent WSJ article highlights a critical alert for beneficiaries who inherited traditional IRAs after 2019: the window to take distributions is limited and time-sensitive. Under the...

By: Angela M. Stockbridge, Esq. As we approach the end of 2025, employers, plan sponsors, and benefits professionals are turning their attention to one of the most important annual updates in the retirement-plan arena: the...

Falcon Rappaport & Berkman LLP (FRB) is pleased to announce that Angela M. Stockbridge has joined the firm as a Partner in its Taxation Practice Group. Angela brings extensive experience in employee benefits, executive...

By: Matthew E. Foreman, Esq., LL.M. and Tonya L. Hurd It’s probably safe to say that anyone with a cell phone or an email account has been the target of a scam, such as phishing, smishing, or quishing.[1] The scammers,...